Catching Up on Tech-Driven Insurance

Why Lemonade (LMND) Leads OSCR, ROOT, and HIPPO in Disruption and Growth Potential

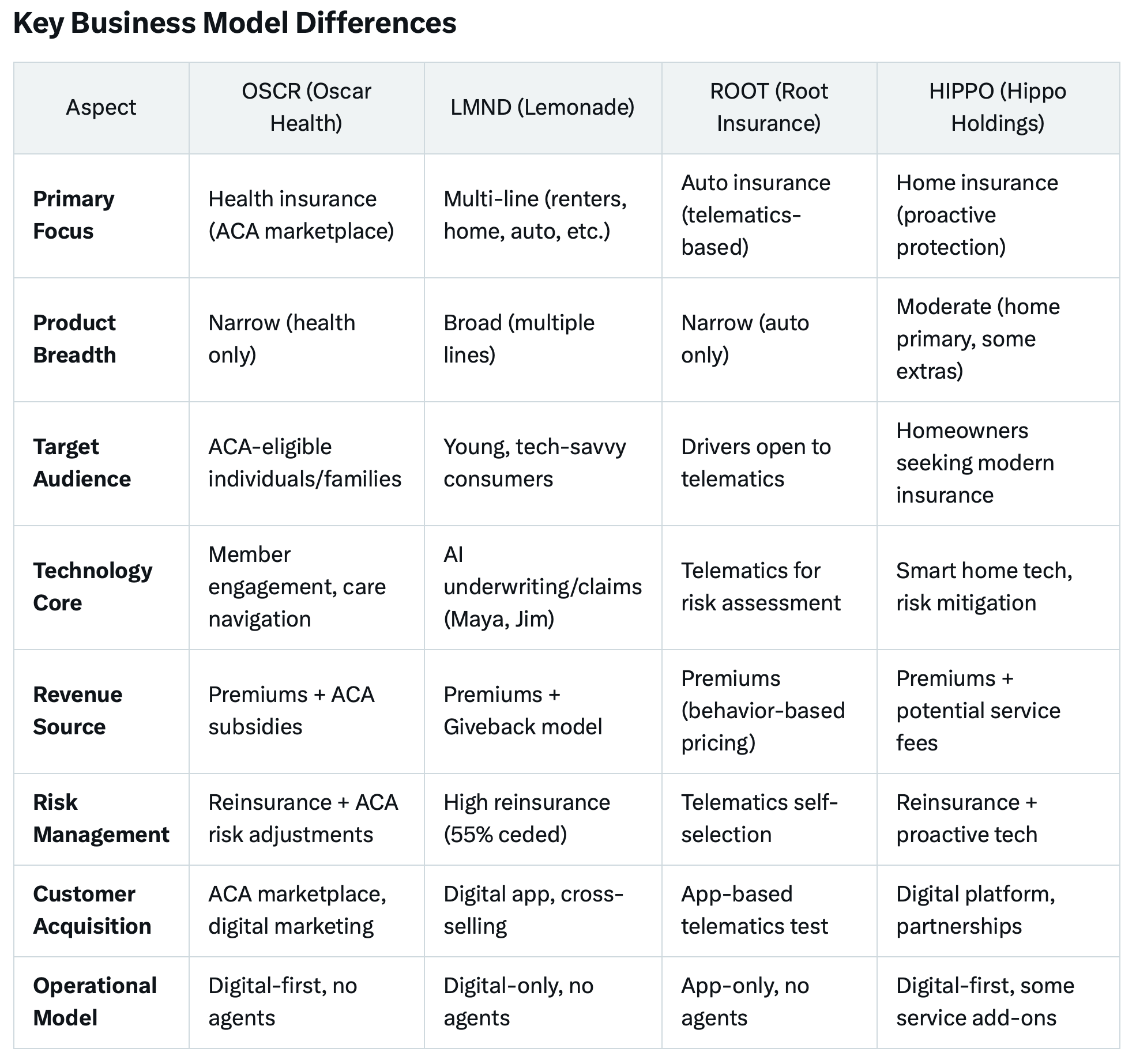

1. Lemonade (LMND) Business Model Overview:

Lemonade is a multi-line insurtech company offering a broad range of property, casualty, and life insurance products. Founded in 2015 and based in New York, NY, LMND uses artificial intelligence (AI) and behavioral economics to streamline the insurance process, targeting a digital-first, younger demographic with a mission to “rebuild insurance from the ground up.”

Core Products:

Renters, homeowners, auto, pet, life, and car insurance, available primarily in the US with a small presence in Europe (e.g., Germany, France, Netherlands). Target Market: Tech-savvy consumers, predominantly under 35, seeking simple, affordable insurance through a digital platform, with over 2.43 million customers as of Q3 2024.

Technology Utilization:

AI Maya: An LLM that handles policy issuance across all product lines, enabling instant coverage.

AI Jim: An LLM that processes claims in as little as two seconds, automating payouts and reducing human intervention.

Proprietary platform “Blender” integrates all operations, using real-time behavioral data (e.g., language, response times), geospatial analysis, and weather data for precise underwriting.

Revenue Model:

Premiums from policyholders, with a significant portion (around 55%) ceded to reinsurers to de-risk operations. A “Giveback” model donates unclaimed premiums to charities chosen by customers, enhancing brand loyalty but not directly contributing to revenue. Key Differentiators: Broad product portfolio allows cross-selling opportunities (e.g., 17% of pet insurance sold to existing renters customers). Heavy reliance on AI for both underwriting and claims, aiming for low operational costs (over 2,000 customers per employee vs. peers’ 250-450). Digital-only, no-agent model contrasts with traditional insurers’ reliance on intermediaries.

Risk Management:

Cedes a higher-than-average 55% of premiums to reinsurers, reducing volatility and capital reserve needs, with plans to lower this as AI models improve and stabilize cash flows (e.g., through life insurance expansion).

2. Oscar Health (OSCR) Business Model Overview:

Oscar Health is a technology-driven health insurance company focused on providing individual and family health plans, primarily through the Affordable Care Act (ACA) marketplace. Founded in 2012 and headquartered in New York, NY, Oscar aims to simplify the healthcare experience for consumers by leveraging data and technology to improve member engagement and reduce costs.

Core Products:

Individual and family health insurance plans (ACA marketplace). Small group plans and Medicare Advantage in select markets.

Target Market:

Individuals and families seeking affordable health insurance, often through government-subsidized marketplaces, with approximately 1.7 million members across 20 states as of December 31, 2024. Technology Utilization: Uses a proprietary platform to enhance member experience with features like telemedicine, personalized care navigation, and a user-friendly app for managing claims and finding providers. Data analytics to optimize care delivery, focusing on high-engagement touchpoints (e.g., 24/7 doctor access via app). Emphasis on transparency and simplicity, contrasting with the complexity of traditional health insurers.

Revenue Model:

Premiums from policyholders, supplemented by government subsidies under the ACA. Aims to reduce medical loss ratios (MLR) through preventative care and technology-driven efficiency, though still reliant on reinsurance to manage risk.

Key Differentiators:

Focuses exclusively on health insurance, a highly regulated and complex market. Prioritizes member experience over pure cost-cutting, aiming to retain customers in a competitive ACA landscape. Less emphasis on underwriting automation compared to property and casualty insurers like LMND, ROOT, and HIPPO; more focus on care coordination.

Risk Management:

Relies on reinsurance to offset high medical claims, typical in health insurance, and operates within ACA risk adjustment programs to balance high-cost patients.

3. Root Insurance (ROOT) Business Model Overview:

Root Insurance is a tech-driven auto insurance company that uses telematics to assess driver risk and price policies based on individual behavior rather than demographics. Founded in 2015 and based in Columbus, OH, ROOT operates in all 50 states, focusing on disrupting the auto insurance market with a data-centric approach.

Core Products:

Auto insurance (personal lines only, no commercial or multi-line offerings).

Target Market:

Drivers willing to share driving data via a mobile app, particularly those who believe they are low-risk and can benefit from behavior-based pricing, with a growing customer base in a $380 billion US auto market.

Technology Utilization:

Telematics via a mobile app tracks driving habits (e.g., braking, speed, time of day) during a test period to set premiums, avoiding traditional factors like age or gender. Machine learning refines risk models, aiming for precision in identifying low-risk drivers. Digital-first platform eliminates agents, focusing on app-based policy management and claims.

Revenue Model:

Premiums from policyholders, with a focus on retaining low-risk drivers to improve loss ratios. Minimal reliance on reinsurance compared to LMND, as telematics aims to inherently reduce risk exposure by targeting safer drivers.

Key Differentiators:

Niche focus on auto insurance with telematics as the core differentiator, unlike LMND’s multi-line approach. Pricing based on actual driving behavior rather than proxies, appealing to safe drivers seeking lower rates. No physical infrastructure or agent network, fully app-based.

Risk Management:

Relies on telematics to self-select low-risk drivers, reducing claims frequency and severity without heavy reinsurance dependence, though this exposes ROOT to market cyclicality and adoption risks.

4. Hippo Holdings (HIPPO) Business Model Overview:

Hippo Holdings is a tech-enabled home insurance company focused on proactive protection rather than just reactive claims handling. Founded in 2015 and headquartered in Palo Alto, CA, HIPPO uses technology to mitigate risks and enhance customer experience in the home insurance market, with some expansion into adjacent lines.

Core Products:

Homeowners insurance (primary focus), with ancillary offerings like auto, pet, and small commercial insurance in select markets.

Target Market:

Homeowners seeking modern, tech-driven insurance with added value (e.g., home maintenance services), targeting a growing segment of the $120 billion US home insurance market.

Technology Utilization:

Smart home technology (e.g., sensors for leak detection, fire prevention) offered free to policyholders to reduce claims, paired with data from satellites and public records for underwriting. Digital platform streamlines policy issuance and claims, though less AI-reliant than LMND or ROOT. Partnerships with home service providers (e.g., maintenance, inspections) enhance value proposition.

Revenue Model:

Premiums from homeowners, with additional revenue potential from partnerships and service fees (e.g., Hippo Home Care). Moderate reinsurance use to manage catastrophe risk, common in home insurance due to natural disasters.

Key Differentiators:

Proactive risk mitigation through smart home tech sets it apart from traditional home insurers and LMND’s broader focus. Smaller product range than LMND, but more specialized than ROOT’s auto-only model. Combines insurance with home protection services, aiming to reduce loss ratios and attract customers.

Risk Management:

Uses reinsurance to offset catastrophe risks (e.g., wildfires, hurricanes), while smart home tech aims to lower claims frequency, balancing reactive and proactive strategies.

Comparative Analysis

Scope and Diversification:

LMND’s multi-line approach offers the most diversification, reducing reliance on a single market compared to ROOT (auto), HIPPO (home), and OSCR (health). This allows LMND to cross-sell and tap multiple revenue streams, a flexibility others lack.

Technology Application:

LMND and ROOT are the most AI- and data-intensive, but LMND applies it across products, while ROOT focuses solely on telematics for auto. OSCR uses tech for engagement rather than underwriting, and HIPPO blends tech with physical devices, a hybrid approach.

Risk Management Strategy:

LMND’s heavy reinsurance (55%) contrasts with ROOT’s reliance on telematics to inherently lower risk, HIPPO’s mix of reinsurance and prevention, and OSCR’s use of ACA mechanisms alongside reinsurance. LMND’s approach prioritizes growth over immediate profitability, while others balance risk differently.

Customer Experience:

OSCR emphasizes healthcare navigation, LMND focuses on speed and simplicity, ROOT targets fairness in pricing, and HIPPO adds value through home protection. Each caters to distinct customer needs within their niches.

Scalability:

LMND’s broad platform is the most scalable due to its multi-line potential. ROOT and HIPPO are constrained by their niches, while OSCR’s scalability is tied to ACA market dynamics and regulatory changes.

Conclusion

The business model differences reflect each company’s strategic focus:

OSCR is a health insurance play with a consumer-centric, regulated model.

LMND is a versatile, AI-driven multi-line insurer with broad growth potential.

ROOT is a specialized auto insurer betting on telematics for precision. HIPPO is a niche home insurer with a proactive, tech-enhanced approach.

In my opinion, LMND’s diversified model offers the most balanced opportunity and provides the greatest long-term growth potential.